Is PTO Payout Taxed? How Vacation Payout Taxes Work

Wondering how your PTO payout is taxed? Learn about federal supplemental wage withholding (22%), FICA, state taxes, and how to calculate your net cash-out.

If you’ve recently left a job or are planning to quit, getting your hands on your final paycheck can feel like a win. You’ve earned that money, and you’re ready to pocket it. But then you look at the pay stub and realize: Wait, where did a third of my vacation payout go?

It’s a common shock. You expect your hourly rate times your unused hours, but the check you actually get is much smaller.

So, is PTO payout taxed differently, and why is the tax rate so high?

Yes, your PTO payout is taxed. But here’s the kicker: it isn’t actually taxed at a higher rate on your final tax return—it’s just withheld at a higher rate when you receive the check. Let’s break down exactly why this happens, how the IRS looks at your vacation time, and how to figure out what you’ll actually take home.

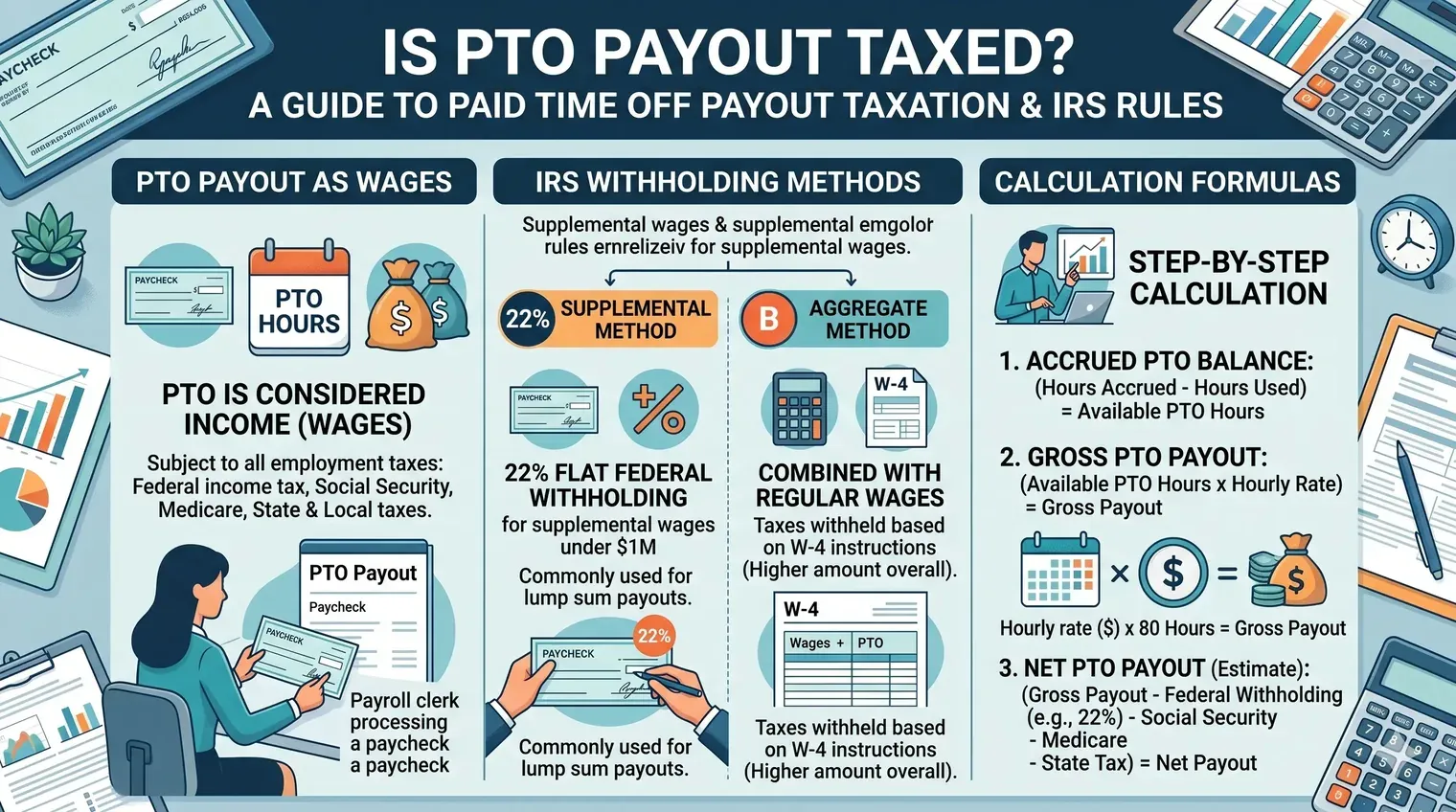

The IRS Rules: Why PTO is “Supplemental”

When you get paid your normal salary or hourly wage, your employer uses tax tables to estimate how much to withhold based on your tax bracket.

But when you get a lump sum for unused vacation time, the IRS looks at it differently. They classify it as supplemental wages.

Supplemental wages are simply payments made to an employee outside of their regular salary. This includes:

- Bonuses

- Commissions

- Overtime pay

- PTO and vacation cash-outs

Because it’s supplemental, the payroll department doesn’t use your normal tax bracket to calculate the withholding. Instead, they use a different method.

The 22% Federal Withholding Rule

For federal taxes, the IRS allows employers to use a flat withholding rate for supplemental wages.

Under current rules, that flat rate is:

22% (Federal Supplemental Tax Rate)This means the moment your employer calculates your PTO payout, they slice 22% off the top for federal income tax.

If your normal federal tax bracket is 10% or 12%, this feels like a massive hit. On the flip side, if you’re a high earner in the 24% or 32% bracket, the 22% rate might actually under-withhold your taxes, meaning you’d owe a little extra at the end of the year.

Other Taxes Taken Out of Your Payout

Federal income tax is just the first deduction. You’ll also see these taxes pulled from your gross payout:

1. FICA Taxes (7.65%)

You still have to pay payroll taxes on your vacation payout. This includes:

- Social Security: 6.2% (up to the annual limit, which is $176,100).

- Medicare: 1.45% (plus an extra 0.9% if you earn over $200,000).

2. State Supplemental Taxes

If your state has an income tax, they’ll want a piece of the pie too. Many states have flat supplemental rates just like the federal government:

- California: 10.23% flat supplemental rate

- New York: 10.90% flat supplemental rate

- Illinois: 4.95% flat supplemental rate

- Texas, Florida, Washington, Nevada, Wyoming, South Dakota, Alaska, Tennessee: 0% (no state income tax)

A Real-World Example: California vs. Texas

Let’s look at how this plays out in real life. Imagine you have a gross PTO payout of $3,000.

Here is what gets withheld depending on where you work:

| Tax Type | California (High Tax) | Texas (No State Tax) |

|---|---|---|

| Federal Supplemental | 22.00% ($660) | 22.00% ($660) |

| FICA (Social Security & Medicare) | 7.65% ($229.50) | 7.65% ($229.50) |

| State Supplemental | 10.23% ($306.90) | 0.00% ($0) |

| Total Withheld | 39.88% ($1,196.40) | 29.65% ($889.50) |

| Your Take-Home Pay | $1,803.60 | $2,110.50 |

As you can see, if you’re in California, almost 40% of your payout disappears into taxes before the check even hits your bank account.

Withholding vs. Actual Tax: You Might Get It Back

Here is the most important thing to understand: withholding is not your final tax rate.

Withholding is just a prepayment to the IRS. When you file your taxes at the end of the year, your PTO payout gets added to your total annual income. Your actual tax rate is calculated based on your final tax bracket.

Why this matters: If your employer withheld 22% for federal taxes, but your actual tax bracket is only 12%, you will get that extra 10% back as a tax refund when you file your tax return in the spring. The money isn’t gone forever; it’s just sitting with the IRS until tax season.

The Alternate Route: The Aggregate Method

Sometimes, your employer won’t use the flat 22% rate. Instead, they’ll use the Aggregate Method.

Under this method, they combine your regular wages and your PTO payout into one single payment. Then, the payroll software calculates your tax withholding as if you earn that massive amount every single pay period.

Because our tax system is progressive, this trick fools the payroll system into thinking you make a lot more money than you actually do, pushing you into a much higher tax bracket for that check. This can result in even more money being withheld than the flat 22% rate.

How to Calculate Your Take-Home Check

If you want a rough estimate of what you’ll actually pocket, you can run the math yourself:

Take-Home Pay = Gross Payout - (22% Fed + 7.65% FICA + Your State Tax)Where:

- Gross Payout = Your Unused PTO Hours × Your Hourly Pay Rate

If you don’t feel like pulling out a calculator, you can check your exact numbers with our free PTO Payout Tax Calculator. Just select your state, put in your salary, and it will do all the heavy lifting for you.

How to Lower Your Taxes on a PTO Payout

If you don’t want the IRS taking a huge chunk of your final check, you have a couple of options. You’ll need to set these up with your HR department before they run your final payroll:

1. Dump it into your 401(k)

Ask your HR department if you can contribute your PTO payout directly to your traditional 401(k). Since this is pre-tax money, you won’t pay federal or state income taxes on it now (though FICA taxes will still be withheld).

2. Put it in an HSA

If you have a Health Savings Account, you can contribute pre-tax dollars to cover future medical expenses. Ask if you can route your payout straight there to keep it tax-free.

The Bottom Line

Your PTO payout will be taxed, and because it is classified as a supplemental wage, your employer will likely withhold a flat 22% federally. However, any over-withholding is just a temporary loan to the government—you’ll get it back as a refund when you file your taxes next year.

Make sure to estimate your check beforehand using our PTO Payout Tax Calculator so you know exactly what to expect on your final day.

Frequently asked questions

4 questions answered

No. Your PTO payout isn't taxed at a higher rate in the long run. It's treated as ordinary income on your tax return. However, it is withheld at a higher flat rate (22% federally) because the IRS classifies it as supplemental wages.

It depends on your state. Federally, employers withhold a flat 22% for supplemental wages, plus 7.65% for FICA (Social Security and Medicare), plus any state supplemental income tax.

Because the IRS forces employers to treat payouts as 'supplemental wages.' This means they withhold a flat 22% federal tax immediately, which is often higher than your normal tax bracket withholding.

Yes, usually. If your employer's plan allows it, you can ask HR to put your final PTO payout directly into your pre-tax 401(k) to defer federal and state income taxes.

About The PTO Payout Research Team

The PTO Payout Research Team is a collective of certified payroll specialists, compensation analysts, and employment data researchers. We build open-source tools and perform rigorous primary-source compliance research to help employees and employers verify final paycheck and PTO payouts accurately.